5 Things to Consider About Taxable Municipal Bonds

There's a small portion of the bond market that investors may have overlooked but now may want to consider—the taxable municipal bond market.

Most municipal bonds pay interest that is exempt from federal and potentially state income taxes. However, interest on some municipal bonds is subject to both federal and state income taxes depending on the taxpayer's location and applicable tax law. These bonds, known as taxable municipal bonds, generally pay higher interest rates than tax-exempt municipal bonds to make up for the lack of tax benefits.

We'll address the primary reasons investors may want to consider taxable municipal bonds, but first let's review the difference between taxable and tax-exempt municipal bonds.

Taxable vs. tax-exempt municipal bonds

Taxable municipal bonds pay interest income that's subject to federal and potentially state income taxes, whereas tax-exempt municipal bonds pay interest income that's generally exempt from federal and state income taxes.

Both taxable and tax-exempt municipal bonds are often issued by the same issuer and don't differ in credit quality. An issuer may choose to issue a bond as either a taxable or tax-exempt issue for a variety of reasons, such as the yield environment or to attract a different investor base to increase demand for their bonds.

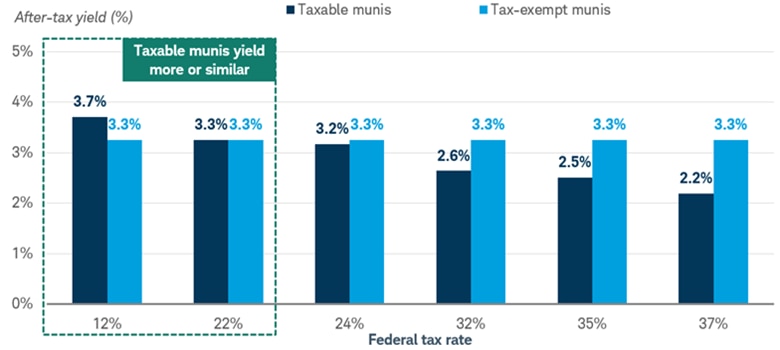

Due to the different tax treatments between taxable and tax-exempt municipal bonds, taxable municipal bonds may be an attractive option for investors in lower tax brackets or for tax-advantaged accounts like an individual retirement account (IRA). Investors in higher tax brackets may still want to consider tax-exempt municipal bonds for taxable accounts, like a brokerage account, as they may yield more than taxable municipal bonds after considering the effects of taxes.

Investors in lower tax brackets may want to consider taxable municipal bonds vs. tax-exempt municipal bonds

Source: Bloomberg, as of 3/25/2026.

Tax-exempt municipal bonds are represented by the Bloomberg Municipal Bond 7 Year (6-8) Index and taxable municipal bonds are represented by the Bloomberg Municipal Index Taxable Bonds Index. Taxable municipal bonds assume a 5% state tax rate and 3.8% Net Investment Income Tax for the 32%-and-above tax rates. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results. For illustrative purposes only.

Five things to know about taxable municipal bonds

1. Taxable municipal bonds offer attractive yields

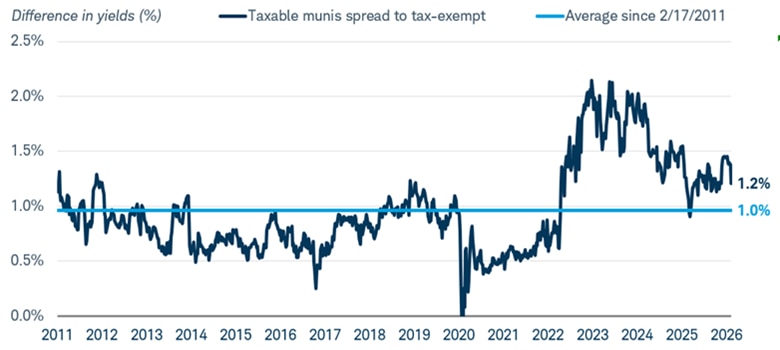

Yields for taxable municipal bonds are attractive, in our view, compared to tax-exempt municipal bonds of similar maturities. For example, since January 2010, on average, an index of taxable municipal bonds has yielded 1.0% more than an index of tax-exempt municipal bonds. Only during a brief period in March 2020 when the market was very volatile due to the onset of the COVID-19 pandemic crisis did taxable municipal bonds yield less than tax-exempt municipal bonds. Although that difference has come down recently, today, it is about 1.2% which is above the longer-term average.

Taxable municipal bonds currently yield about 1.6% more than tax-exempt municipal bonds

Source: Bloomberg, weekly data from 2/17/2011 to 3/26/2026.

Difference in yield-to-worst between the Bloomberg Municipal Index Taxable Bonds Intermediate-term Index and the Bloomberg Municipal Bond 7 Year (6-8) Index. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For illustrative purposes only.

2. Taxable municipal bonds are generally high in credit quality

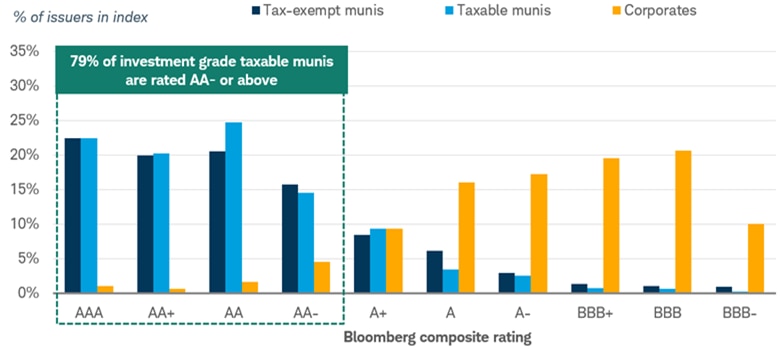

Another potential benefit of taxable municipal bonds is that they're generally higher in credit quality than other alternatives. For example, 79% of the taxable municipal market is rated in the top four rungs of credit quality–AA minus or above.1 This compares to 82% for the tax-exempt municipal market and only 8% of the corporate market, as illustrated in the chart below.

Most taxable municipal bonds currently are very high in credit quality

Source: Bloomberg, as of 3/26/2026.

Tax-exempt municipal bonds are represented by the Bloomberg Municipal Bond Index, taxable municipal bonds are represented by the Bloomberg Municipal Index Taxable Bonds Index, and corporates are represented by the Bloomberg US Corporate Bond Index.

Based on the number of issuers in each index. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For illustrative purposes only.

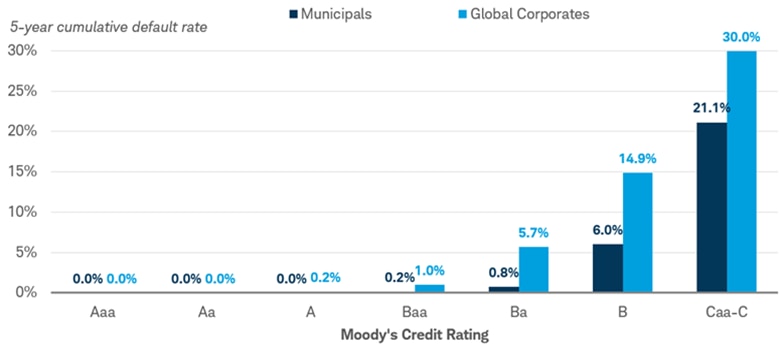

This is notable for investors because higher-rated issuers tend to default—that is, to miss an interest or principal payment—less frequently than lower-rated issuers. For example, in a study that spanned 1970 to 2024, 0.2% of Baa rated municipal bonds defaulted, according to Moody's Investors Service. During the same period, lower-quality B rated municipal bonds defaulted over 30 times more often, at a rate of 6.0%.

Moreover, municipal bond issuers, which include issuers of taxable municipal bonds, tend to default less frequently than corporate bond issuers. Looking at the Baa rated cohort, the default rate for municipal bonds was 0.2%, compared with 1.0% for corporates.

Default rates have been lower for municipal bonds compared to corporates

Source: Moody's Investors Service, as of 8/4/2025.

This is the most recent data available. "US municipal bond defaults and recoveries, 1970 – 2024".

The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. For illustrative purposes only.

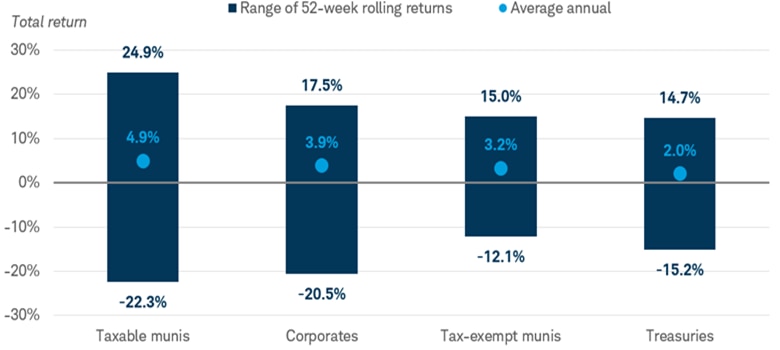

3. Taxable municipal bonds historically have performed well

Since the start of 2010, an index of taxable municipal bonds had returned an average annual total return of 4.9% outpacing corporates, Treasuries, and tax-exempt municipal bonds. However, this is an average and can substantially vary by year. For example, as shown in the chart below, the best 52-week total return for taxable municipal bonds was just shy of 25% while the worst 52-week total return was just over -22%. In other words, on average, total returns for taxable municipal bonds are better than corporate tax-exempt municipal bonds and Treasuries, but the volatility is greater too. Total return is composed of the yield that an investor receives as well as any price fluctuations. The yield component has generally been the largest driver of total returns over time. This bodes well for future total returns because yields today are elevated and can help buffer any negative price changes.

Taxable municipal bonds historically have returned more than some other fixed income investments

Bloomberg, using weekly data from 1/1/2010 to 3/20/2026.

Tax-exempt municipal bonds are represented by the Bloomberg Municipal Bond Index, taxable municipal bonds are represented by the Bloomberg Municipal Index Taxable Bonds Index, corporates are represented by the Bloomberg US Corporate Bond Index, and Treasuries are represented by the Bloomberg US Treasury Bond Index. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For illustrative purposes only.

However, taxable municipal bonds do have some risks. Here are two of the most prominent:

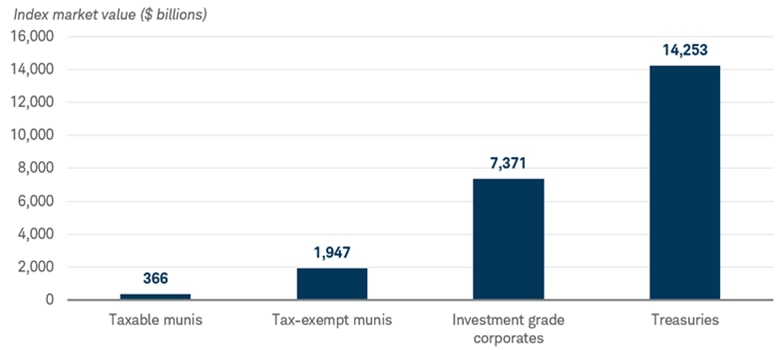

4. The relatively small size of the market could pose liquidity problems

The amount of newly issued taxable municipal bonds has been declining recently. Couple this with the fact that the taxable municipal market is much smaller than many other fixed income markets, as illustrated in the chart below, and investors may have a hard time finding enough taxable municipal bonds to achieve adequate diversification. Additionally, smaller markets are generally less liquid than larger ones, like the Treasury market, which means that it can be more difficult to sell your bond if you need to. Therefore, we suggest that if you're considering taxable municipal bonds, plan on holding them until maturity. The smaller market and lower liquidity of taxable municipal bonds is also an issue for investors in funds like exchange-traded funds (ETFs) or mutual funds.

Due partly to the size of the market, there aren't many mutual funds or ETFs that invest solely in taxable municipal bonds. In fact, there is only one open-ended ETF that we know of that invests in taxable municipal bonds and doesn't use leverage. Leverage generally means using borrowed funds to try to amplify returns. However, leverage can also amplify negative returns. Bonds that are less liquid are generally more volatile in times of market stress.

The size of the taxable municipal market can pose additional risks

Source: Bloomberg, as of 3/26/2026.

Taxable municipal bonds are represented by the Bloomberg Municipal Index Taxable Bonds Index , tax-exempt municipal bonds are represented by the Bloomberg Municipal Bond Index, investment grade corporates are represented by the Bloomberg US Corporate Bond Index, and Treasuries are represented by the Bloomberg US Treasury Index. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For illustrative purposes only.

5. The taxable municipal index is sensitive to interest rate changes

First, the taxable municipal index has a longer average duration—which makes it more sensitive to changes in interest rates—than the tax-exempt index. For investments such as ETFs or passively managed mutual funds that simply track the index, investors are taking on greater interest rate risk with taxable municipal bonds compared to tax-exempt municipal bonds. This is important because if rates rise , total returns for taxable municipal bonds may underperform their tax-exempt counterparts even more.

What to consider now

For investors in high tax brackets, we generally don't see value in taxable municipal bonds. However, investors in lower tax brackets or those investing a tax-sheltered account like an IRA may want to consider a small allocation to taxable municipal bonds to complement their other fixed income holdings. However, be aware that the size of the market can make it difficult to invest in.

Schwab clients can log in to their accounts and search for individual taxable municipal bonds. If you need additional help, reach out to a Schwab Fixed Income Specialist.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

About the author