Q2 Surprises and What Could Surprise in Q3

Markets tend to be forward-looking. When the outlook changes due to a surprise, it can prompt significant moves in the markets. The second quarter of this year was full of surprises. Let's look back at what surprised the markets in the second quarter and what may be in store for the third quarter.

1. Indexes up but average stock down

In the second quarter stock indexes posted gains while the average stock in the index posted a loss. For the S&P 500, the index was up 4.3% in the second quarter while the average stock in the S&P 500 was down -2.6% (measured by the equal-weighted index). This was also true around the world, the MSCI ACWI Index (All Country World Index) was up 2.4% while average stock in the global benchmark was down -1.7% in the second quarter. This phenomenon is very rare, only having happened five times in the past 30 years. This divergence is fueled by mega-cap Artificial Intelligence (AI) stocks, such as Nvidia and Microsoft. Without exposure to those AI highflyers, it's possible that investors may have lost money last quarter. Considering high concentration of performance in AI in the second quarter, what might be the risks to the market in the third quarter tied to that very narrow leadership? Investors might look to mitigate this concentration risk; stock markets in Europe, Japan, Canada and India have only about 7% exposure to AI-related stocks.

Index up, average stock down in Q2

Source: Charles Schwab, Bloomberg data as of 7/1/2024.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

2. Emerging Market stocks outperformed

With China's weak economy, elevated trade risks, and the strong U.S. dollar it would seem Emerging Market (EM) stocks faced headwinds in the second quarter. Yet they modestly outperformed the S&P 500. These gains were driven by:

- Investors' strong interest in artificial intelligence stocks boosted the EM index's biggest sector (Information Technology) and stock Taiwan Semiconductor Manufacturing Company (TSMC). AI beneficiaries such as TSMC, Samsung Electronics, SK Hynix and Hon Hai Precision Industry (commonly known as Foxconn) make up 16% of the MSCI Emerging Markets Index.

- India's strong growth continued in the second quarter; India's Central Statistics Office at the end of May released an updated 2024 GDP growth estimate of 8.2%. India remains on a path to surpass Japan and Germany and become the world's third largest economy by 2027, according to IMF estimates. India's stocks make up 19.2% of the MSCI Emerging Market Index with those stocks growing 10.3% in the second quarter.

- Stabilization of China's economic growth, balanced between weak consumer demand and stronger export production, resulted in a peak gain of 18% for the MSCI China Index during the quarter. However, the market slid after May 20 following an underwhelming announcement by the Chinese government meant to prop up the property sector. Chinese stocks have been alternating between optimism about an economic recovery to disappointment over the slow pace of improvement and lack of powerful stimulus to revive consumer demand. The Third Plenum a major meeting held roughly once every five years for the purpose of mapping out the general direction of the country's long-term social and economic policies, will be held from July 15-18 and may yield some incremental reforms with potential to surprise the market, but there is no expectation for any major changes. The regular Politburo meeting, a gathering of the top Chinese party officials who oversee the party and central government, is at the end of July, with another opportunity for an announcement for additional spending or debt issuance plans, but again markets do not seem to be expecting anything big.

The outperformance by EM in the second quarter highlights the benefit of having a small strategic asset allocation to EM; trying to time when certain asset classes come in and out of favor can be difficult.

EM outperforms in Q2

Source: Charles Schwab, Bloomberg data as of 7/11/2024.

Performance is normalized, or indexed to zero, on 4/1/2024. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

3. Election outcomes

The surprise call for an election by the French President after his party suffered big losses in the European parliamentary elections in early June led to a sell-off in French stocks and a rise in the risk premium on French debt, fueled by fears the far-right would win a majority and impose costly spending plans widening the budget deficit. According to media outlets, the far-left and the centrist coalitions coordinated with each other in three party run off races to block the far-right from winning a majority. This resulted in a surprise pickup of the largest number of seats by the far-left, although the number fell short of a majority. The outcome may mean any major legislative changes are unlikely, as the leaders of all three groups have vowed not to work together on domestic policy.

French election impact

Source: Charles Schwab, Bloomberg data as of 7/11/2024.

Past performance is no guarantee of future results.

Markets began to reverse June's losses after the first round of voting on June 30, as the margin of victory by the National Rally appeared insufficient to claim a majority in the second round. But the surprise outcome leaves some uncertainty as to what comes next, which may weigh on France's markets. French stocks trade at about 13 times earnings, below their 10-year average of 15, seemingly braced for some domestic political uncertainty. French stocks measured by the MSCI France Index were down YTD 1.4% at the end of second quarter, with the overall MSCI Europe index up 6.4% in the same period. The MSCI France index has already begun to recover post-election in the first two weeks of the third quarter.

It is noteworthy that about 85% of the sales of French companies in the MSCI France Index are not domestic, given France's global brands like LVMH and L'Oreal and Airbus among many others. While the election posed some short-term domestic risk, its mainly the global economic backdrop which over the medium-term could surprise in the third quarter with possible gains on a boost from ECB rate cuts and better growth in Europe overall.

4. Economic surprises turned negative

The quarter began with surprisingly strong global economic data that widely exceeded economists' expectations, reflected by a positive economic surprise index which measures how economic data fares relative to economists' expectations. But the data for the United States, Europe and some other major countries gradually worsened relative to expectations during the second quarter, and the quarter ended with the data generally missing forecasts and pulling the economic surprise index below zero. While surprisingly weak economic data is generally not welcomed by markets, the news might increase the likelihood of central banks rate cuts lending support to the stock market. Now that the market is pricing a high likelihood of two rate cuts for both the Fed and European Central Bank (among other central banks) later this year, further negative economic data surprises in the third quarter may be less tolerated by stock market investors.

Economic surprises turn negative

Source: Charles Schwab, Bloomberg data as of 7/10/2024.

Past performance is no guarantee of future results.

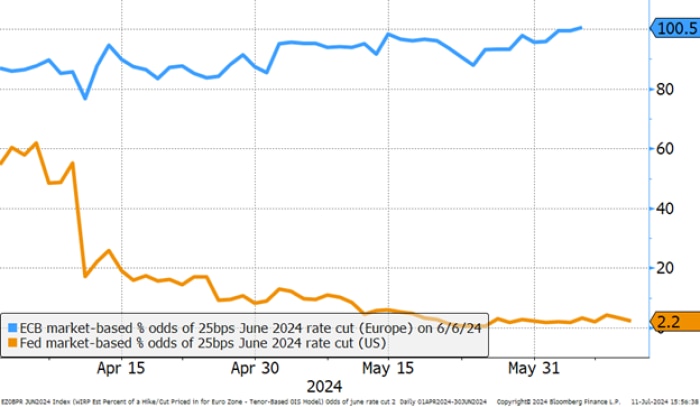

5. No rate cuts by Fed even as ECB and other did start to cut

The European Central Bank, and the central banks of Sweden, Switzerland, and Canada cut rates in the second quarter—but not the Fed. At the start of the second quarter, the interest rate futures market had priced in a greater than 50% chance of a rate cut by the Fed in June and a 95% likelihood of cut by the July meeting. No rate cut took place in Q2 and those July odds now stand at less than 10%. The surprise shift in expectations was in part due to the stronger than expected U.S. economic data for much of the quarter (economic surprise index above zero) along with still relatively easy financial conditions. As noted above, early in the third quarter, markets are now pricing in two rate cuts from the Fed and ECB—but those expectations are subject to a high degree of uncertainty surrounding developments that could influence monetary policy, leaving plenty of room for surprises.

Odds of June rate cut diverged in the run up to the central bank meetings

Source: Charles Schwab, Bloomberg data as of 7/11/2024.

Past performance is no guarantee of future results.

Surprises

Market surprises tied to market concentration, China, elections, economic data, and central bank actions may also be potential drivers of volatility in the markets in Q3. Investors might consider adding a portfolio review and assessing potential exposures to their list of summer plans.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

About the author